Portrait of a fraudster - what to look out for

Why do people commit fraud?

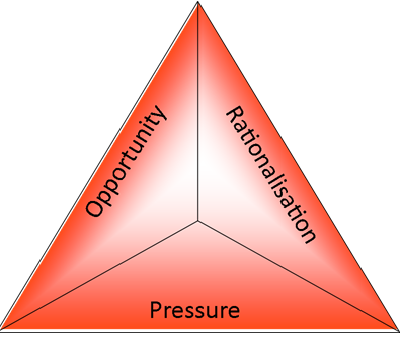

Cressey's Fraud Triangle is a model for explaining the factors that cause someone to commit fraud. It consists of three components which normally must all be present for fraudulent behaviour to occur:

Opportunity i.e. the circumstances that permit someone to commit a fraud, is generally provided through weaknesses in internal control systems such as inadequate or lack of:

- Supervision and review

- Separation of duties

- Management approvals

- System controls

Pressure i.e. the pressure placed on or incentive provided to a person to commit fraud, can be imposed due to:

- Personal financial problems

- Personal vices such as gambling, drugs, extensive debt, etc.

- Unrealistic deadlines and performance goals

Rationalisation occurs when the individual develops a justification for their fraudulent activities i.e. they have a frame of mind or character that allows them to commit a fraud. The rationalisation varies by case and individual. Some examples include:

- "I really need this money and I'll put it back when I get paid"

- "I'd rather have the organisation on my back than the tax office or creditors"

- "I just can't afford to lose everything – my home, car, everything"

- "The organisation deserves this for treating me badly"

- "I am entitled to the money"

- "I am underpaid, or my employer cheats me"

- "My employer is dishonest to others and deserves to be fleeced"

NOTE: the above fraud triangle does not apply in situations where a "predatory employee" is involved i.e. a person who takes a job with the prime intent of committing fraud against his/her employer.

What is a "red flag" of fraud and corruption?

A red flag is a set of circumstances that are unusual in nature or vary from normal activity. It is a signal that something is out of the ordinary and may need to be investigated further. Red flags do not indicate guilt or innocence but merely provide possible warning signs of fraud.

Conducting a review after a fraud is detected may show that red flags were present. If the warning signs had been recognised, then the loss may not have occurred or may have been substantially reduced.

Studies of fraud cases have consistently found the existence of red flags which were either not recognised or were recognised but not acted upon by anyone. Red flags should lead to some kind of appropriate action, however, their existence does not automatically mean that a fraud has occurred. One needs to recognise the difference and remember that responsibility for follow-up and investigation of red flags should be placed in the hands of measured and responsible persons. In such cases, the matter should first be brought to the attention of a line manager, or if unsure, advice should be sought from the Integrity and Standards Unit (ISU).

What are some red flags to look out for?

- "Red-flagging the white collar criminal" - This document provides examples of red flags that either on their own or in combination with others, may indicate possible fraudulent activity in the workplace.

- "Red flags when dealing with third parties" [PDF 85.7kb] - This document attached here provides a list of red flags which may indicate a heightened risk of corrupt behaviour.